Free Courses Sale ends Soon, Get It Now

Free Courses Sale ends Soon, Get It Now

The Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR, 2020), was notified by the Central Board of Indirect Taxes and Customs. It came into force from 21st September 2020. CAROTAR 2020 (“Rules”) aims to add to the existing operational certification procedures which are prescribed under different trade agreements such as Free Trade Agreements (FTAs), Preferential Trade Agreement, Comprehensive Economic Cooperation Agreement and Comprehensive Economic Partnership Agreement.

Over the years in India, there has been a staggering reduction in the preferential duties under FTAs and an increase in the preferential trade volumes. Frequent instances of misuse by the fraudulent traders who have mis-declared the country of origin of imported goods to avail undue duty concession has come to the Government’s notice.

Accordingly, to curb the misuse, Section 28DA of the Customs Act, 1962 was inserted by clause 110 of the Finance Act, 2020. This section provides for due diligence on the part of an importer to satisfy that the originating criteria’ requirements are met. The importer needs to have sufficient origin related information on imported goods and submitting just the Certificate of Origin is not enough.

The Central Government notified CAROTAR 2020 as required under Section 28DA of the Customs Act. An importer should do due diligence before importing the goods to ensure that they meet the prescribed originating criteria. CAROTAR requires an importer to satisfy himself that the importing goods meet the prescribed originating criteria and do basic due diligence before importing them.

CAROTAR 2020 is effective from 21st September 2020. The rules listed down in CAROTAR 2020 are as follows.

Rule 3 – Preferential tariff claim

The importer or his agent should make a declaration in the bill of entry that they qualify as originating goods to claim the preferential rate of duty under the respective agreement when filing a bill of entry. The importer also needs to produce the certificate of origin covering each item claimed under the preferential duty rate.

The importer needs to enter the following details of the certificate of origin in the bill of entry –

The claim of the preferential rate of duty can be denied without verification if the certificate of origin is

Rule 4 – Origin related information to be possessed by the importer

Any importer who wishes to claim preferential rate of duty should possess information as indicated in Form I of the Rules and submit the same, when requested, to the proper officer. Form I provides a list of basic minimum information that the importer should know while claiming the preferential rate of duty for importing goods.

The importer should have all the supporting documents related to Form I for a minimum of 5 years from filing the bill of entry. He should exercise reasonable care for ensuring the truthfulness and accuracy pertaining to the information and documents obtained by him relating to Form I.

Rule 5 – Requisition of information from the importer

During the course of customs clearance, the proper officer may seek information and documents from the importer in terms of Rule 4, if he has reason to believe that the origin criteria prescribed in the respective Rules of Origin are not met. The importer needs to furnish information and documents to the proper officer on requisition within ten days from the date of such request.

When the proper officer is satisfied that the respective Rules of Origin are met based on the documents and information obtained from the importer, he shall inform the same in writing within fifteen days to the importer. If the importer cannot provide the required information and documents or it is found insufficient to conclude that the origin criteria are met, the proper officer will forward a verification proposal to the nodal officer appointed in terms of Rule 6.

Rule 6 – Verification request

All requests for verification under this rule are made through a nodal officer as designated by the Board. The proper officer may request for verification of certificate of origin from the Verification Authority when-

The proper officer may deny the claim of the preferential rate of duty without further verification. He can deny the claim when –

Rule 7 – Identical goods

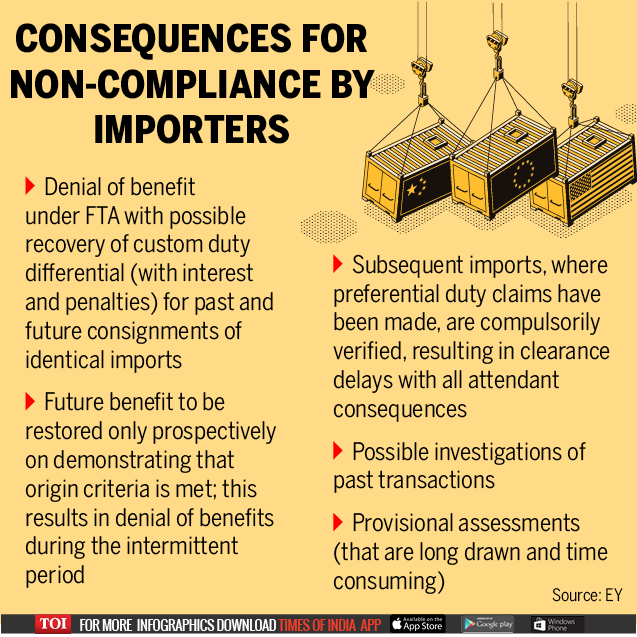

When it is determined that an importer’s goods do not meet the origin criteria as prescribed in the Rules of Origin, the Commissioner of Customs or the Principal Commissioner of Customs can reject claims of the preferential rate of duty for identical goods imported by the importer from the same exporter or producer. The Commissioner of Customs or the Principal Commissioner of Customs can reject claims for identical goods filed prior to or after the determination of rejected goods imported by the same exporter or producer without any further verification.

When a claim is rejected on identical goods, the Principal Commissioner of Customs or the Commissioner of Customs can restore the preferential tariff treatment on identical goods with prospective effect. He can restore it if the exporter or producer modifies the manufacturing or other origin related conditions to fulfil the origin requirements of the Rules of Origin under the trade agreement.

The CAROTAR provides the minimum basic information that the importer needs to know before importing goods. These rules help the importer to ascertain the country of origin, assist Customs Authorities in the smooth clearance of import of goods under FTAs and claim concessional duty. It strengthens the hands of the Customs for checking any misuse of the duty concessions under FTAs.

© 2024 iasgyan. All right reserved