Free Courses Sale ends Soon, Get It Now

Free Courses Sale ends Soon, Get It Now

Disclaimer: Copyright infringement not intended.

Context

What is Digital Lending?

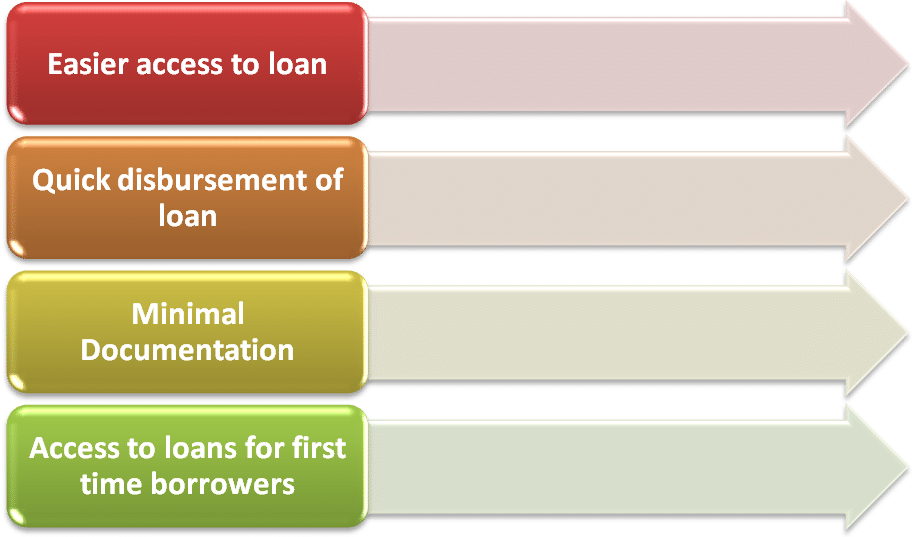

Benefits of Digital lending

New norms

Future of Lending Is Digital

https://epaper.thehindu.com/Home/ShareArticle?OrgId=GM4A4S5V5.1&imageview=0

© 2024 iasgyan. All right reserved