Free Courses Sale ends Soon, Get It Now

Free Courses Sale ends Soon, Get It Now

Disclaimer: Copyright infringement not intended.

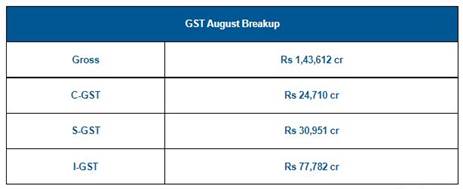

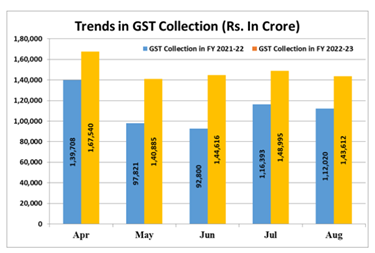

Context

What do the improved revenues signify?

Performance of the states

End of Compensation Regime

Read about Basics of GST in detail here: https://www.iasgyan.in/daily-current-affairs/goods-and-services-tax-gst

Read about Basics of GST Compensation Scheme in detail here: https://www.iasgyan.in/daily-current-affairs/gst-compensation-38

Recommendations of 47th GST Council Meeting

I.Recommendations relating to GST rates on goods and services

|

S. No. |

Description |

From |

To |

|

|

GOODS |

||||

|

1. |

Printing, writing or drawing ink |

12% |

18% |

|

|

2. |

Knives with cutting blades, Paper knives, Pencil sharpeners and blades therefor, Spoons, forks, ladles, skimmers, cake-servers etc |

12% |

18% |

|

|

3. |

Power driven pumps primarily designed for handling water such as centrifugal pumps, deep tube-well turbine pumps, submersible pumps; Bicycle pumps |

12% |

18% |

|

|

4. |

Machines for cleaning, sorting or grading, seed, grain pulses; Machinery used in milling industry or for the working of cereals etc; Pawan Chakki that is Air Based Atta Chakki; Wet grinder; |

5% |

18% |

|

|

5. |

Machines for cleaning, sorting or grading eggs, fruit or other agricultural produce and its parts, Milking machines and dairy machinery |

12% |

18% |

|

|

6. |

LED Lamps, lights and fixture, their metal printed circuits board; |

12% |

18% |

|

|

7. |

Drawing and marking out instruments |

12% |

18% |

|

|

8. |

Solar Water Heater and system; |

5% |

12% |

|

|

9. |

Prepared/finished leather/chamois leather / composition leathers; |

5% |

12% |

|

|

10. |

Refund of accumulated ITC not to be allowed on flowing goods: i.Edible oils ii.Coal |

|||

|

|

Services |

|||

|

11. |

Services supplied by foreman to chit fund |

12% |

18% |

|

|

12. |

Job work in relation to processing of hides, skins and leather |

5% |

12% |

|

|

13. |

Job work in relation to manufacture of leather goods and footwear |

5% |

12% |

|

|

14. |

Job work in relation to manufacture of clay bricks |

5% |

12% |

|

|

15. |

Works contract for roads, bridges, railways, metro, effluent treatment plant, crematorium etc. |

12% |

18% |

|

|

16. |

Works contract supplied to central and state governments, local authorities for historical monuments, canals, dams, pipelines, plants for water supply, educational institutions, hospitals etc. & sub-contractor thereof |

12% |

18% |

|

|

17. |

Works contract supplied to central and state governments, union territories & local authorities involving predominantly earthwork and sub-contracts thereof |

5% |

12% |

|

|

|

|

|

|

|

B.Other GST rate changes recommended by the Council

|

S. No. |

Description |

From |

To |

|

Goods |

|||

|

1. |

Ostomy Appliances |

12% |

5% |

|

2. |

Orthopedic appliance- Splints and other fracture appliances; artificial parts of the body; other appliances which are worn or carried, or implanted in the body, to compensate for a defect or disability; intraocular lens |

12% |

5% |

|

3. |

Tetra Pak (Aseptic Packaging Paper) |

12% |

18% |

|

4. |

Tar (whether from coal, coal gasification plants, producer Gas plants and Coke Oven Plants. |

5%/18% |

18% |

|

5. |

IGST on import of Diethylcarbamazine (DEC) tablets supplied free of cost for National Filariasis Elimination Programme |

5% |

Nil |

|

6. |

Cut and Polished diamonds |

0.25% |

1.5% |

|

7. |

IGST on specified defence items imported by private entities/vendors, when end-user is the Defence forces. |

Applicable rate |

Nil |

|

Services |

|||

|

1. |

Transport of goods and passengers by ropeways. |

18% |

5% (with ITC of services) |

|

2 |

Renting of truck/goods carriage where cost of fuel is included |

18% |

12% |

C Withdrawal of exemptions

C1. Hitherto, GST was exempted on specified food items, grains etc when not branded, or right on the brand has been foregone. It has been recommended to revise the scope of exemption to exclude from it prepackaged and pre-labelled retail pack in terms of Legal Metrology Act, including pre-packed, pre-labelled curd, lassi and butter milk.

C.2 In case of the following goods, exemption from GST will be withdrawn:

|

S. No. |

Description of goods |

From |

To |

|

GST rate changes |

|||

|

1. |

Cheques, lose or in book form |

Nil |

18% |

|

2. |

Maps and hydrographic or similar charts of all kinds, including atlases, wall maps, topographical plans and globes, printed |

Nil |

12% |

|

3. |

Parts of goods of heading 8801 |

Nil |

18% |

C.3 In case of the following goods, the exemption in form of a concessional rate of GST is being rationalized:

|

S. No. |

Description of goods |

From |

To |

|

GST rate changes |

|||

|

1. |

Petroleum/ Coal bed methane |

5% |

12% |

|

2. |

Scientific and technical instruments supplied to public funded research institutes |

5% |

Applicable rate |

|

3. |

E-waste |

5% |

18% |

C4. In case of Services, following exemptions are being rationalized:

|

S. No. |

Description

|

|

1. |

Exemption on transport of passengers by air to and from NE states & Bagdogra is being restricted to economy class |

|

2 |

Exemption on following services is being withdrawn. a. Transportation by rail or a vessel of railway equipment and material. b. storage or warehousing of commodities which attract tax (nuts, spices, copra, jaggery, cotton etc.) c. Fumigation in a warehouse of agricultural produce. d. Services by RBI,IRDA,SEBI,FSSAI, e. GSTN. f. Renting of residential dwelling to business entities (registered persons). g. Services provided by the cord blood banks by way of preservation of stem cells

|

|

3. |

Like CETPs, common bio-medical waste treatment facilities for treatment or disposal of biomedical waste shall be taxed at 12% so as to allow them ITC |

|

4. |

Hotel accommodation priced upto Rs. 1000/day shall be taxed at 12% |

|

5. |

Room rent (excluding ICU) exceeding Rs 5000 per day per patient charged by a hospital shall be taxed to the extent of amount charged for the room at 5% without ITC. |

|

6. |

Tax exemption on training or coaching in recreational activities relating to arts or culture, or sports is being restricted to such services when supplied by an individual. |

D. GST on casinos, race course and online gaming

The Council directed that the Group of Ministers on Casino, Race Course and Online Gaming re-examine the issues in its terms of reference based on further inputs from States and submit its report within a short duration.

E .Clarification on GST rate

E1. Goods

E2 .Clarification in relation to GST rate on Services

Other miscellaneous changes

The rate changes recommended by the 47th GST Council were made effective from 18th July, 2022.

https://indianexpress.com/article/explained/august-2022-gst-collection-significance-8125104/

© 2024 iasgyan. All right reserved