Free Courses Sale ends Soon, Get It Now

Free Courses Sale ends Soon, Get It Now

Disclaimer: Copyright infringement not intended.

Context

Background

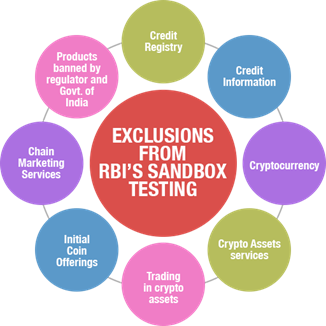

Regulatory Sandbox

|

List of innovative products/services/technology which could be considered for testing under RS are as follows.

Innovative Products/Services

Retail payments

Money transfer services

Marketplace lending

Digital KYC

Financial advisory services

Wealth management services

Digital identification services

Smart contracts

Financial inclusion products

Cyber security products

Innovative Technology

Mobile technology applications (payments, digital identity, etc.)

Data Analytics

Application Program Interface (APIs) services

Applications under block chain technologies

Artificial Intelligence and Machine Learning applications . |

Objectives

Regulatory Sandbox: Benefits

The setting up of an RS can bring several benefits, some of which are significant and are delineated below:

Evidence on benefits and risks of product

Helps check Viability of product before wide scale roll out

Helps in financial inclusion

Enables evidence-based regulatory decision-making

Reduced costs and improved access to financial services

Interoperable Regulatory Sandbox

|

Determination of Dominant Feature Two sets of factors would be considered on deciding the dominant feature. Firstly, the type of enhancement to the existing products like loans, deposits, capital market instruments, insurance, G-sec instruments and pension products. And secondly, the number of relaxations sought by the entity for undertaking the test under the IoRS. The dominant feature would be decided with greater weightage to the number of relaxations sought. |

Special cases

A Global Perspective

The way forward

© 2024 iasgyan. All right reserved