Free Courses Sale ends Soon, Get It Now

Free Courses Sale ends Soon, Get It Now

Disclaimer: Copyright infringement not intended.

Context

Background

MUST READ ARTICLES

REPO RATE AND MONETARY POLICY COMMITTEE:

MANAGING INFLATION:

https://www.iasgyan.in/rstv/perspective-managing-inflation

The recent decision

|

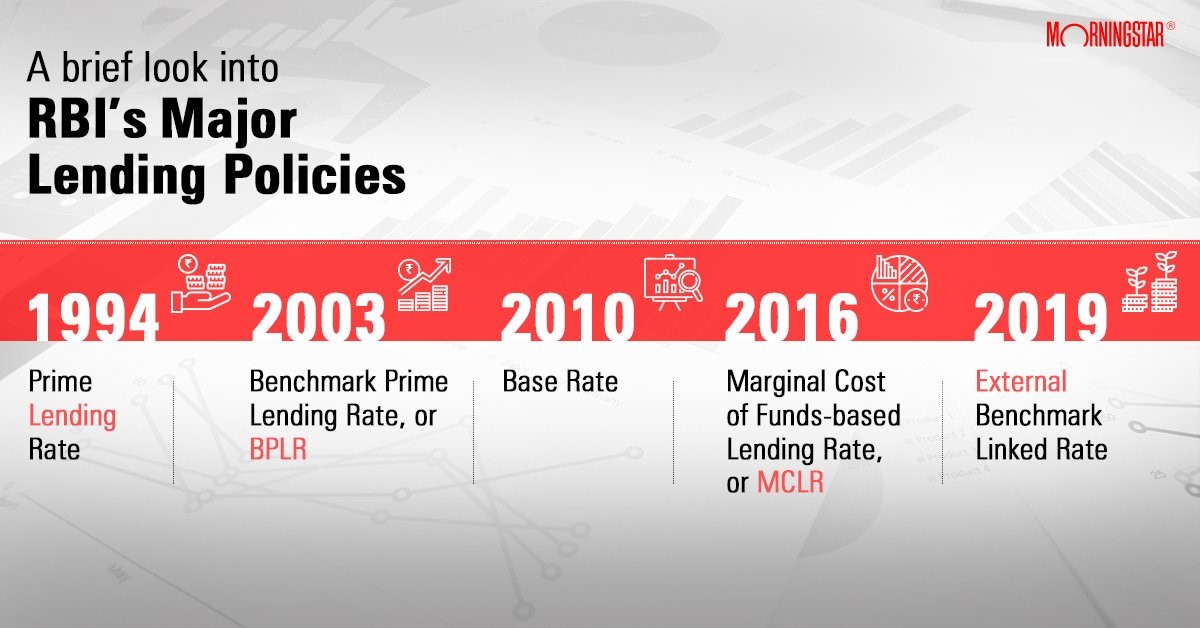

Primary Lending Rate (PLR)

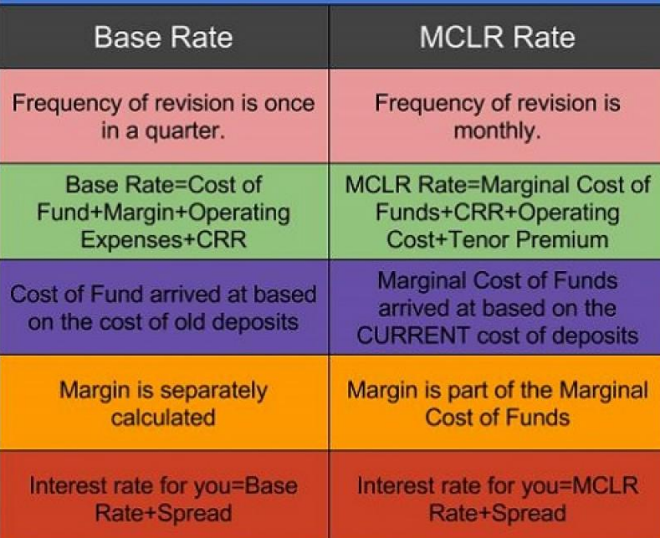

Base Rate Regime (BRR)

1. Cost of Funds (COF)-Banks usually borrows money from RBI, Household Individuals and from the companies. Hence, once banks borrows the money from these entities, definitely bank has to give certain interest rate on these deposits right? Hence, assume your bank is giving you a 7% interest on your FD, then the bank has to consider this cost of 7% while deciding the lending rate. 2. Operational Expenses (OE)-When bank lend money to a borrower or collect money from depositors, the bank will incurre certain expenses. Obviously, such expenses should be part of the lending rate and have to incurred by the borrower. 3. Cost of CRR (Cash Reserve Ratio which Banks keeps with RBI)-Assume that Bank collected Rs.100 Crore from the bank. As per RBI guidelines, Bank has to keep certain portion of this with the RBI, which in finance world called as CRR or Cash Reserve Ratio. Assume that this is around 4%. Hence, if the bank collected Rs.100 Cr from the depositors, then bank has to keep Rs.4 Cr with RBI. This Rs.4 Crore which is RBI will not earn a single interest to Bank. Because RBI will not give any interest on CRR. Hence, if the Bank collected Rs.100 Cr at the promise of giving an interest rate of 7% to individuals, then this cost of Rs.4 Cr which is IDLE with the RBI is also the cost of the Bank itself. Bank has to bear this 7% interest on Rs.4 Cr from its pocket and give to the depositor. This is called as Cost of CRR. Hence, RBI guidelines included considering this Cost of CRR while deciding the lending rate. 4. The margin of Profit-After considering the above expenses, bank at the end of the day has to run it’s show as a business entity. Hence, they have to consider what margin of profit they are looking at in their business. Such a margin of profit also is part of the lending rate. Combined all the four parameters, banks used to fix their lending rate under the Base Rate Regime (BRR). Hence, as per RBI guidelines, the lending should not be at any cost below this base rate. Do remember that banks were also allowed to charge certain additional interest rate over and above this base rate. Such additional rate is called as SPREAD or PREMIUM. This usually be lower to high creditworthy borrowers and obviously high for lower creditworthy borrowers. The spread or premium is introduced because the bank giving a loan to an individual is entirely different than a loan to business entity. Hence, based on the risk in lending, banks can set their spread or premium to the borrower. Marginal Cost of Lending Rate (MCLR) With the introduction of Base Rate based lending regime, RBI thought whenever there is a change in policy rate by RBI, the lending rate will also reduce in the same proportion. Such change is called a Monitory Policy Tranmission or MPT. Bank expected that if the rate has fallen, then the lending rate also must fall equally. Assume that RBI reduced the interest rate for around 50 BPS (100 BPS-1%), then RBI expects banks will also reduce the lending rate by 50 BPS. If banks reduce it, then it is called as the efficient transmission of RBI policy. If not, then it is called inefficient transmission. What RBI noticed is that such efficient transmission is not happening in the Base Rate pricing method of lending. Hence, RBI introduced the MCLR effective from 1st April 2016. MCLR is usually arrived at based on below mentioned four considerations. 1) Marginal Cost of Funds: This is the cost of CURRENT borrowing to the bank. You noticed in based rate system that banks used to arrive at the cost of the fund as per their comfort. Also, they used to consider the existing deposits rates as if the cost of fund. However, in the case of MCLR based loans, the last month deposit rates (current, savings, term deposits etc) will be considered to arrive the cost of funds. Banks not only consider the current borrowing cost but also their margin of profit is also included in this Marginal Cost of Funds. This is called as the Return on Networth. The return on net worth is nothing but the bank’s profit they want to earn from their lending business. You might be noticed that in the case of base rate system, the cost of fund and margin was used to calculate separately. However, in case of MCLR based loans, both cost of fund and margin (return on net worth) are together are called Marginal Cost of Funds. The calculation of this Marginal Cost of Funds is as below. Marginal cost of funds = Marginal cost of Borrowing X 92% + Return on Net worth X 8% Notice the above formula, the stress or the higher priority to arrive at Marginal Cost of Funds is to cost of borrowings (the deposits banks accepted) than the return on net worth or margin. 2) Negative Carry on Cash Reserve Ratio- As I pointed above, banks have to keep a certain level of their deposits with reserve bank. This is the safety measure and banks will not earn any interest on this amount. Banks have to keep a certain level (4% as on April 5, 2016) of their deposits with the Reserve Bank. This ratio is the Cash Reserve Ratio (CRR). Banks don’t earn any interest on the amount. Essentially, they can use 96% of the deposits for lending and the remaining 4% does not earn the bank anything. RBI allows some leeway for this with adjustment to the Hence, such cost is also considered to arrive at MCLR calculation. 3) Operating Costs- Apart from the cost of deposit and CRR, banks also have to incur some expenses. Such expenses are called as Operating costs. Such cost may include salaries, rent or other overhead expenses. 4) Tenor Premium/Discount- If the bank is lending for higher tensors (like home loans), then there are uncertainties associated which are not factored in the MCLR calculated based on (say) 1-year MCLR. Therefore, the banks will charge a premium to the borrower for the risk (uncertainty) associated with lending for higher tenor loans. Hence, this tenor premium is usually higher for long tenure loans. Considering all the above four factors, Banks arrive at the MCLR rate. What is the concern with MCLR-based system?

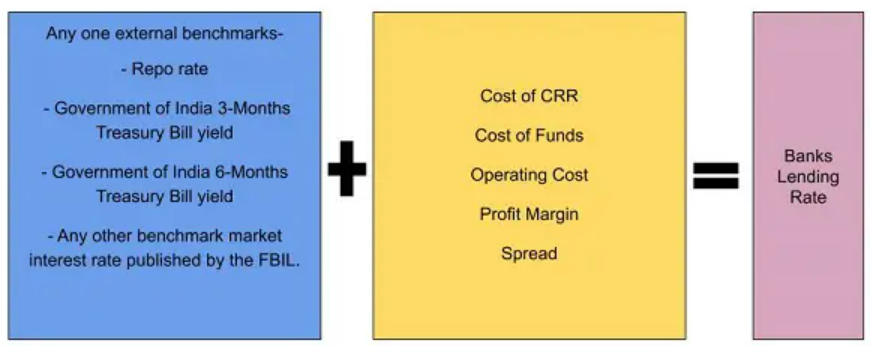

All about External Benchmark Lending Rate After the introduction of MCLR, RBI was skeptical about the implementation of MCLR by banks. Hence, RBI set up a committee which is known as Janak Raj Committee. Janak Raj Committee came out with certain interesting findings and they are as below.

Hence, considering all these aspects, the Committee recommended shifting to external benchmark lending rate rather than banks internally decide their benchmark. This is where the RBI acted now and introduced all loans be under external benchmark lending rate effective from 1st October 2019. How does the new system work?

How will it benefit borrowers?

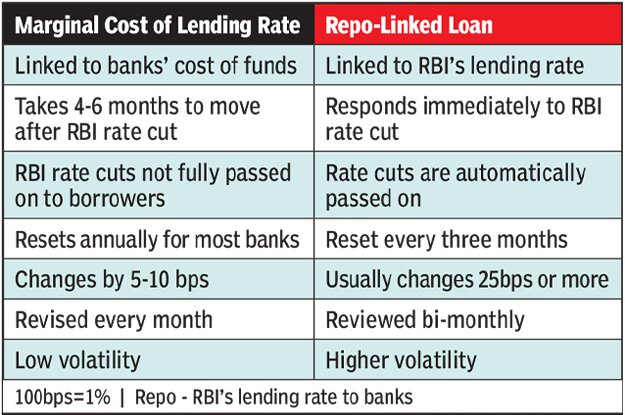

Unlike earlier benchmarks – Base Rate and Marginal Cost of funds-based Lending Rate (MCLR) – External Benchmark-linked Lending Rate (EBLR) ensures better transmission of policy rate changes. In case of a repo rate cut, banks have to pass on the entire benefit to borrowers. Likewise, borrowers will have to bear the entire burden of any repo rate hike. RBI's Monetary Policy Report points to a more effective transmission of policy action under the EBLR regime.

Personal loans and other retail loans, as well as loans to small businesses, have floating interest rates based on EBLR. Banks can opt to provide such loans linked to the EBLR to other categories of loans too. Banks have to follow the same external benchmark for a particular loan category. This has been done so that the borrowers can get transparent, standardised, and easy-to-understand loan products. In a nutshell, Why a Shift from IBLR to EBLR? Several issues with the IBLR (Internal Benchmark Lending R ate) have led to the shift to EBLR. Some of these have been listed below.

Benefits of EBLR for the Borrowers and the Banks The EBLR rate benefits the borrowers and the lending banks in several ways.

|

Reasons for the pause

|

ACCOMMODATIVE MONETARY POLICY Accommodative monetary policy is when central banks expand the money supply to boost the economy. Measures taken are meant to make money less expensive to borrow and encourage more spending. |

Growth projection

Inflation forecast

|

PRACTICE QUESTION Q. Which of the following statements are correct in reference to the External Benchmark Lending Rate system? a) Rate cuts are automatically passed on. b) Reviewed half-yearly. c) Responds immediately to RBI rate cut. d) Janak Raj Committee had recommended EBLR. 1. a and c 2. b and d 3. a, c and d. 4. None of the above. Correct Answer: Option 3 |

READ ALL ABOUT RBI: https://www.iasgyan.in/daily-current-affairs/rbi

© 2024 iasgyan. All right reserved