In order to create a common rate structure for hospitals, India's Insurance Regulatory Development Authority (IRDAI) must either propose its own regulatory agency to the medical sector or allow hospital regulation.

The inflation rate for hospitalization is currently around 10- 15%, and it was found that the rates are changing regularly.

Important point About (problems related to the hospital's current fee structure):

Different tariffs: Hospitals change rates on a regular basis. There is no agency that regulates pricing and classification. When Covid struck the country last year, patients were overcharged by several hospitals.

Health insurance premium: If the insurance company keeps paying at the hospital's request, the health insurance business will not be successful in the long run. The industry has already recorded a large number of bills.

Individual hospital integration process: Today, healthcare systems and private insurers have separate hospital integration processes that replicate different activities and contribute to inefficiencies and duplications.

No infrastructure to regulate hospitals: IRDAI currently does not have the infrastructure to regulate hospitals. Hospital regulation is a difficult task for IRDAI, as medical care is a government The Indian Insurance Regulatory Development Bureau (IRDAI) is a legal entity established under the Parliamentary Law.

Suggestions of the Panel:

Even with rising penetration, general and medical inflation must be taken into account, and medical inflation far exceeds CPI (Consumer Price Index) inflation, so a correction cycle is needed from a price perspective.

IRDAI has proposed a harmonization of its own common hospital registration, inclusion process, hospital classification, and packaging costs to facilitate standardization and effective use of medical infrastructure under insurance programs.

It is advisable to have a common integrated portal that can be used by all systems / insurers with standardized integration standards (and) it is very difficult to focus specifically on standard safety and quality parameters.

Need to regulate Health Sector:

Healthcare has become one of India's largest sectors in terms of sales and employment.

Population growth, income growth, infrastructure growth, heightened awareness, insurance policy, and the rise of India as a hub for medical tourism and clinical trials are contributing to the development of India's medical sector.

As the demand in this area grows, it becomes important to provide modern medical facilities.

Government-funded health insurance allows the poor in India to receive timely care without the burden of paying for themselves.

Importance of health insurance:

This is a mechanism that pools India's high capital expenditures (OOPE) to provide better financial protection from health shocks.

Health insurance prepayment has proven to be an important tool for pooling risk and protecting against catastrophic (and often poor) costs from health shocks.

In addition, prepaid pool funds can improve medical

The state of life is unevenly distributed: Since independence, people's life expectancy has increased from 35 to 65 years. However, living conditions are unevenly distributed in different parts of the country. India's health problems remain a major concern.

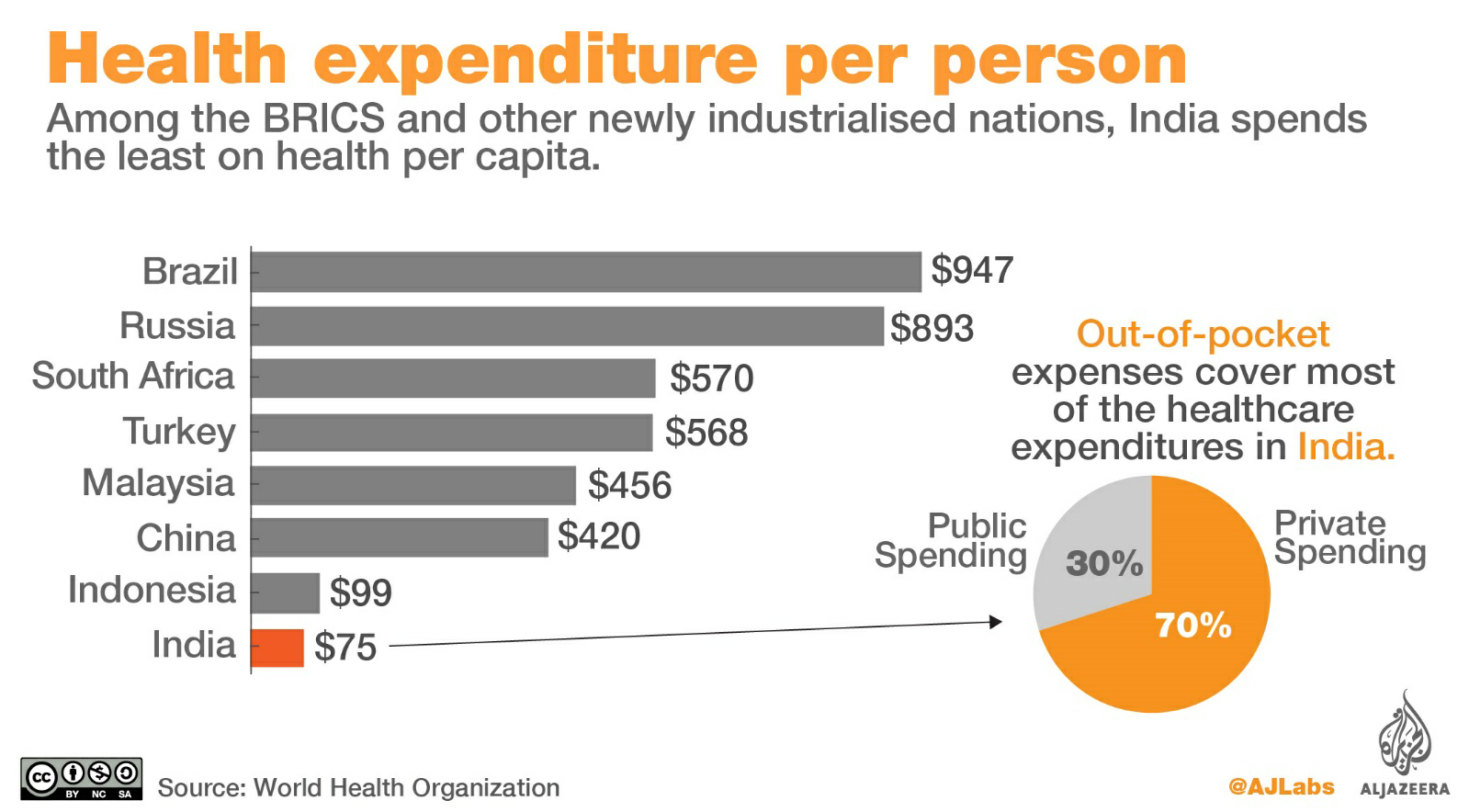

Low government spending: The low government health costs limit the capacity and quality of public sector health services.

A considerable population is overlooked: At least 30% or 40 million people do not have financial protection for their health.